Login

Login

Too many 401(k) providers make it harder than necessary for employers to total and evaluate their 401(k) plan fees for ”reasonableness” – an important fiduciary responsibility - by not charging simple fees. One of these 401(k) providers is the payroll company ADP. Two weeks ago, I described my process for totaling ADP’s 401(k) fees using their DOL-mandated 408b-2 fee disclosure. Now, I’d like to do the same thing for Paychex - ADP’s largest payroll competitor.

Like ADP, Paychex fails to disclose the dollar amount of revenue sharing payments they collect from 401(k) plan investments in their 408b-2 disclosure – they instead force employers to total these 401(k) fees themselves using a spreadsheet. What makes the Paychex 408b-2 worse than its ADP counterpart, however, is its language and length. While the ADP 408b-2 is plain-spoken and short, the Paychex disclosure is written in legalese and almost SIX TIMES LONGER!

If you’re an employer with a Paychex 401(k) plan, I want to help you total your Paychex fees – because I know you’re probably paying higher fees than you think. Below is the 3-step process I use to total Paychex’s 401(k) fees when comparing them to our fees. You can use the same process to total your Paychex fees. I’ll use an actual Paychex 401(k) plan as an example. Once done, you’ll be ready to evaluate the full cost of your Paychex 401(k) plan – including the dollar amount paid by revenue sharing - for reasonableness.

Step #1 – Confirm your Paychex 408-b2 covers all of your 401(k) plan fees

Paychex provides all 3 of the major 401(k) plan administration services – asset custody, participant recordkeeping and Third-Party Administration (TPA). For this reason, the firm is considered a “bundled” 401(k) provider. Paychex’s administration services are described in the Part Two: Services and Fiduciary Status section of their 408b-2 disclosure. In addition, Paychex may also provide investment advice. If they do, this service will also be described in their 408b-2.

If your 401(k) plan retains an independent (non-Paychex) financial advisor, you’ll need to review their 408b-2 disclosure to ensure they don’t charge separate fees. Paychex often pays an independent advisor’s fees from the revenue sharing they collect, but not in all cases. If not, you will need to add the advisor fees to Paychex’s fees when totaling your plan fees.

Step #2 – Total Paychex’s direct fees

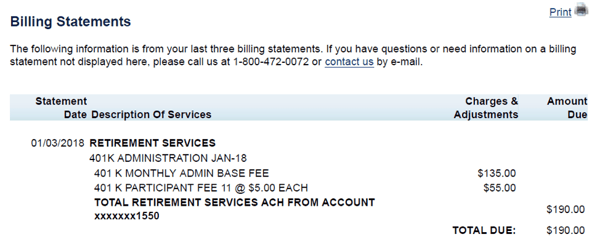

“Direct fees” are the most transparent type of 401(k) provider fee. Their dollar amount must be reported in 408b-2 disclosures and reported in 404a-5 (participant) fee disclosures, plan statements, and Form 5500s when paid from plan assets.

A description of Paychex’s direct fees can be found in section A.1. of Part Three: Fee and Other Compensation Detail and Examples. However, Paychex does not disclose the dollar amount of direct fees in their 408b-2. Instead, Paychex discloses their direct fees in monthly invoices. Below is an example. To total Paychex’s annual direct fees, you must multiply the monthly invoice amount by twelve. I found my Paychex 401(k) plan example paid $2,280.00 ($190.00*12) annually:

Step #3 – Total Paychex’s revenue sharing payments

Revenue sharing is much less transparent than direct fees. It can be estimated in 408b-2 disclosures, buried in the fund expense ratios of 404a-5 disclosures, and disregarded altogether in plan statements or Form 5500s. This lack of transparency makes revenue sharing payments easy to overlook. For this reason, revenue sharing is often called “hidden 401(k) fees.”

However, overlooking the revenue sharing payments made by your 401(k) plan would be a mistake because they reduce participant returns just like direct fees – which means you have a fiduciary responsibility to keep their dollar amount in check too.

To total Paychex’s revenue sharing, you must convert the revenue sharing percentages disclosed in the Schedule A - Investment Related and Revenue Sharing Detail of your 408b-2 to a dollar amount. Below are the steps I take to do it:

- Enter all plan investments, including their current balance, into a spreadsheet.

- For each fund, enter the revenue sharing percentage reported in the Total Annual Revenue Sharing (bps or $ per Participant)** column.

- Multiply each fund’s balance by its revenue sharing percentage to determine the dollar amount the fund pays Paychex in revenue sharing.

- Sum the revenue sharing paid by all plan funds

Using a spreadsheet, I found my Paychex 401(k) plan example will pay $795.46 in revenue sharing annually based on current fund balances:

|

Fund Name |

Expense Ratio |

Balance |

Rev Share % |

Amount |

|

TF BR LP IDX 2020 PX |

1.59% |

$20,355.77 |

0.40% |

$81.42 |

|

TF BR LP IDX 2030 PX |

1.60% |

$15,790.51 |

0.40% |

$63.16 |

|

TF BR LP IDX 2035 PX |

1.60% |

$55,966.16 |

0.40% |

$223.86 |

|

TF BR LP IDX 2040 PX |

1.61% |

$36,928.40 |

0.40% |

$147.71 |

|

TF BR LP IDX 2045 PX |

1.61% |

$28,810.84 |

0.40% |

$115.24 |

|

TF BR LP IDX 2050 PX |

1.61% |

$20,849.90 |

0.40% |

$83.40 |

|

MFS INTL VAL RET PX |

1.98% |

$2,121.82 |

0.40% |

$8.49 |

|

FNKLN S M CP GWTH PX |

2.05% |

$1,601.76 |

0.40% |

$6.41 |

|

VAN S CP INDX RET PX |

1.53% |

$16,441.70 |

0.40% |

$65.77 |

|

AC EQT GRWTH PX |

1.77% |

$12,128.97 |

0.00% |

$0.00 |

|

DFA INF PRTCTD PX |

1.57% |

$3,833.67 |

0.00% |

$0.00 |

|

HF SC GRWTH PX |

2.06% |

$29,308.08 |

0.00% |

$0.00 |

|

TAM INTL EQT PX |

2.09% |

$1,388.39 |

0.00% |

$0.00 |

|

PR MC VAL III PX |

2.01% |

$10,749.00 |

0.00% |

$0.00 |

|

DFA EM PRT PX |

2.02% |

$12,502.87 |

0.00% |

$0.00 |

|

Total |

|

$268,777.84 |

|

$795.46 |

Please note – If Paychex rebates the revenue sharing they collect using “401(k) fee levelization”, your Schedule A may not include a Total Annual Revenue Sharing (bps or $ per Participant)** column. That was my experience when I reviewed a recent Paychex 408b-2 disclosure. Presumably, this column is missing because Paychex rebates 100% of the revenue sharing payments they collect – netting these 401(k) fees to zero. I guess you’re supposed to trust that Paychex is doing that.

Don’t overlook revenue sharing when evaluating your 401(k) plan fees!

When I added the direct fees and revenue sharing paid by my Paychex example, I found the plan paid $3,075.47 in total Paychex fees – $2,280.00 in direct fees and $795.46 in revenue sharing. However, that’s not the end of the story. Because the revenue sharing payments are based on a percentage of assets, their dollar amount will increase automatically as plan assets grow. By the time my Paychex example hits $1M in assets, revenue sharing payments will jump from $795.46 to $2,959.57 – increasing Paychex’s total fees to $5,239.57!

If your Paychex 401(k) plan pays revenue sharing, you overlook look these 401(k) fees at your peril – because they can easily result in excessive fees – especially as your plan grows. While it’s possible to total these fees, the Paychex 408b-2 disclosure doesn’t make this job easy. Too much trouble? I’ve got a simple solution. Replace Paychex with a 401(k) provider that charges simple fees. There’s a good chance you’ll reduce your total plan fees in the bargain!